Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Capital News Today CSPAN March 30, 2011 11:00pm-2:00am EDT

11:00 pm

they are scheduled e-mail directly to you. >> on his last day on the job, the inspector of tarp give his assessment on the 2008 program to stabilize financial markets. he said the program has encouraged large firms to become even bigger and that the government has not seceded in helping struggling homeowners. the house oversight committee also heard a defense of the tarp program from the treasury assistant secretary for financial stability. this is two hours and 20 minutes.

11:01 pm

[captioning performed by national captioning institute] [captions copyright national cable satellite corp. 2011] >> thank you for the opportunity to appear before you today. it is a pleasure and an honored to appear before the subcommittee on my final day as special inspector general. it is hard to believe that two and a half years ago there was assisting a star, certainly no such thing as a tarp subcommittee. after an outpouring than doubling of government funds to a financial industry that was teetering on the brink of collapse, accompanied by historic riverside, emergency economic stabilization act, which greeted tart, also created sig tarp. i am proud to say that, since our inception in 2008, we have made progress in fulfilling the

11:02 pm

goals set before us by congress. we should 9 quarterly report, 13 audits, secured civil or criminal charges against more than 50 individuals, 18 different defendants have been convicted of tarp-related fraud, and our investigations have helped assist in the recovery of or the prevention to loss in a some of $70 million. as importantly -- of $17 million. as importantly, we brought in to retool a program desperately in need of it. tarp made promises to both wall street and to ministry. i'm fortunate, its track record has been mixed. it fulfil this -- unfortunately, its track record has been mixed. it fulfilled its promise to wall street, but it has failed to live up to its promises to main street.

11:03 pm

when treasury give out billions the -- billions of dollars to banks, it did so without policy in place to accomplish that goal, without any strings to require lending or provide incentives for it. not surprisingly, credit continued to contract throughout the financial crisis and well into the recovery. second, the promise to preserve home ownership, such an important part of the legislative are in the treasury struck with congress in order to get top past lies in tatters. the original promise to modify up to $700 billion in mortgages that treasury was to purchase under tarp was cast aside within weeks. it was replaced months later with the promise by this administration to modify 4 million mortgages for struggling

11:04 pm

homeowners. that promise has, too, been cast aside. the cold start reality of a failed program that was poorly designed, poorly managed, poorly executed, and will come nowhere close to coming to the original promise. after secretary paulson and then secretary geithner told the world that they would stand by and not let our largest banks fail, and demonstrated that they were ready, willing to enable to use the term funds to accomplish that, we were left with the financial system -- the tarp funds to accomplish the, we were left with the financial system that was more dangerous than the ones that created the crisis. it is a promise that looks like it, too, will go unmet. notwithstanding the passage of frank, there's still the

11:05 pm

perception that the government will bail out large banks. should the hit the rocks again, the united states government will come to their rescue. it still remains theoretically possible that it will address of too-big-to-fail. treasury and the regulators would get into broad powers and authorities to take on the largest banks. these are the same regulators whose incompetence and lack of foresight was prescribed by the financial -- described by the financial regulatory committee as the reason for the crisis. without dramatic and quick action, i am afraid that this promise, too, will be broken

11:06 pm

with potentially devastating consequences. i think you for the opportunity to be here today. i also want to thank you and the chairman of the full committee for your strong support over the years. we would not have been able to accomplish in nearly any of our goals or our accomplishments if it were not for the strong continues and, above all, bipartisan support from congress. if we received only support from one side or the other, it would not have had nearly the impact that your uniform support has been for our office. i think you. i also want to thank the incredible men and women who worked at tarp for their sacrifices, their commitment, and they demonstrate all the good that is in federal workers. it has been my privilege and honor to work with them for the last two years plus. a look forward to answering any questions you may have. -- i look forward to entering

11:07 pm

any questions you may have. >> thank you. you have mentioned in your report, in your editorial today in "the new york times" that the objectives of tarp had been shifted dramatically in two and a half years since the creation of the program. it is now evolving, but it seems like, if they fail to meet metrics set for themselves, they change the metrics. can you elaborate on this? >> it happened far too often with this program that, when a goal was not met, rather than do what you would expect in a good government program, which is that you have a goal and doucette policy to achieve that goal, measure performance against that goal, and if you are not performing, you change the program, make the necessary changes to accomplish that goal. far too often, in tar, and it has been to set a goal, treat no

11:08 pm

policy to achieve that goal, basically ignored, try not to be transparent about the progress toward that goal. when you do not meet that goal, changeable and then declare mission accomplished and move on. -- changed that the goal and then declare mission accomplished and move on. it happened with a lot of the main street goals which have been written out. recently, a treasury official talked about these incredibly important mean streak goals that were part of the bargain, for white tarp got past, and dismissed them as window dressing. they were intended to be more than that. those are some of the broken promises i discussed in the op ed and in our reports. >> to go further on this, there has been a discussion in recent days that part has been a success for the taxpayers. in dollars and cents terms, it has not been a huge negative.

11:09 pm

what is the legacy of tarp and this unprecedented intervention in the market? >> there is a number of areas where tarp fell short of course, there are the goals that were not met. there is a cost to not meeting your main street bulls. one of them is in the impact of government credibility. the bottom line is that the people do not trust their government could part of the reason is tha -- government. part of the reason is because they do not meet their goals. gradus legacies is the failure to deal with -- greatest legacy is the failure to deal with too-big-to-fail. it exacerbated the problem of too-big-to-fail. it was no longer as explicit as

11:10 pm

it could be. the whole reason why tarp contribute to avoiding the economic collapse was because of the promise that we would not let these institutions fail. that has had the unintended consequences of the problem of getting bigger and bigger, more concentrated. you mentioned the statistical data that backs up what we all know, that they're able to borrow money more cheaply, able to access the credit markets, access capital markets, and they are more systemic the significant than they were before, if for no other reason that there are fewer of them and they are bigger than ever. >> dodd-frank prevented that from happening? >> it was not a magic wanted it did not actually change the status quo. it gave one possible path of the deregulators could choose to use to potentially accomplish that goal, but the bill itself is just that, a bill. unfortunately, based on the market's perception, they are

11:11 pm

very much and convinced that it will be used in the effective way that it would need to be used in order to really address too-big-to-fail. >> even in the design of the bill, does it leave wide openings for bailouts to continue? >> technically, under the letter of the law -- and there is some dispute about what the meaning of all this is -- in certain language, bailout will not happen. but that sort of ignores reality. the reality is that, when we talk about too-big-to-fail, far too often we lose sight of the fact of what those words mean. it means really what they say. whether there is a law in the books or not, if we had a repeat of the financial crisis, it will not matter what the law in the books is because its failure is not an option. you cannot let those banks fail if that happens. it does not matter what your political or personal ideology is.

11:12 pm

the country will go down. there will be a systemic crash. there will be devastating consequences. the point is that, much like the tarp, whoever happens to be president at the time and controlling congress at that time, for the best of the country, has to go in and rescue the banks. it is not a moral question. that is what too-big-to-fail means. certain transportation's of the bill gives certain degree of discretion as to which -- certain portions of the build a certain degree of discretion as to dollars and something you can point to that does not mean an orderly bankruptcy and can continue in the form of a bailout, whether funded by the industry or elsewhere, if you have a to-be-to-filled eyes, we will be right back where we were in 2008 -- too big -- too-

11:13 pm

big-to-fail crisis, we will be back where we startewere in 200. unless and until they use those the 40's, we are worse than the status quo. -- the use those -- use those authorities, we are worse than the status quo. the market is looking at dodd- frank and they are rejecting it. it increases capital requirements. the volcker rule, although a lot of exceptions have been made to defeated, these are all hopeful in certain areas of potential risk. but the big ticket question we're talking about it, does it solve too-big-to-fail? the answer is not yet.

11:14 pm

in terms of what the direction has been, i am not entirely optimistic that it will. >> thank you. we recognize mr. quigley. >> thank you, mr. chairman. it is not that i disagree with you on the point. but i want to understand better. you advocating your testimony today and in your editorial, discussing the recommendation to supply our strength, -- to simplify or make smaller. the risk-taking will shift elsewhere in the system were is harder to regulate.

11:15 pm

think hedge funds. what is your response to that? >> that sounds like an embracing a too-big-to-fail. >> i do not think he is correct. >> this is similar to a different argument. our largest banks are not of the size and scope that they are. they will not able to compete with larger european banks. if we break that down, what it really means is that, ok, so other countries guarantee their banks and those banks haven't advantage. unless we guarantee our banks, our banks will not able to compete with those other banks. that is essentially what it comes down to. so the question becomes are you willing to believe that the government should subsidize and guarantee financial institutions or do you believe that we should be true to our capitals ideals and let these banks compete without an economic subsidy, a very significant subsidy that

11:16 pm

they receive? sure, there are a number of doomsday scenarios that one could posit, that if we actually use the tools of dodd-frank and we were true to the idea of ending too-big-to-fill, it may result in banks that are not as profitable as they are today. >> but there are instances in which unfair trade practices, for example, by other countries do put our capitalistic ideals at risk. you do not see that as a possibility in the banking industry? >> i think is a possibility, but there are other ways to deal with those policy concerns rather than embracing the idea that we should be effectively granting our largest banks a subsidy. and essentially putting them on the books. there's very little difference when you compare where we were in the lead up to the financial crisis with fannie mae and freddie marked -- and freddie mac than where we are right now. is an explicit guarantee. it creates distortions on the

11:17 pm

market. in many ways, we could end up in that same exact situation. sure, the banks can reach short- term profits because they can compete with other banks that have subsidies. but i will take the other side. if we remove these subsidies, if we remove the implicit guarantee overtime, we will have a healthier and better banking system. this is what chairman ben bernanke said recently. this is what larry summers said recently. >> how do you protect our banks in the meantime from unfair practices or unfair competition as it might exist? >> there is constant interaction. >> i do not think that you have to like to-be-to-fail or embrace it to be concerned about that potential risk, right? >> right. but there are whole of this is dedicated to dealing with foreign offices and foreign regulators through the g-20. that is the right place to do

11:18 pm

with them and not throwing your hands up and say that we will subsidize our largest banks and take money out of one pockets and bridget one pocket and put it into the pockets of the shareholders. that is what is happening. $34 billion was one of the dollar subsidies that we give to our largest banks as an implicit guarantee. i say take the money and put it elsewhere. i think we will be better off. >> i appreciate that. i guess the second point is that what is implied here that encourages banks to engage in risky behavior, can you detail the risky behavior you see today? >> sure. the idea of risky behavior is that banks -- anybody who has a bank, especially when they are large, interconnected in simi buses, they will make decisions on how to invest their money, how they manage their portfolio, and the question is on the level of risk they will attach to each of those decisions. the problem with too-big-to-fail

11:19 pm

is that it impacts of that decision-making process. senator kaufman, when he was the chair of the congressional oversight panel, described it as being the rational decision of an executive when you take out the -- and what to big to fail does is take the bottom of that because it is the rational assumption that, if the risk does not work out, you will not have negative consequences of that risk. that is what happens with too- big-to-fail to and you actually rationalize risky behavior because it is in the dusty -- best interest of the bank and the shareholders and executives. >> thank you. >> mr. man for five minutes. >> thank you, mr. chairman. orofsky formr. brodsk

11:20 pm

looking at this issue in such a scope, a tremendous challenge to our country when it happened, but the health the capacity to then look back at what happened and as the kinds of difficult questions that allow us to consider the implications of all that happened so quickly with such remarkable significance at the height of the challenge to our financial system. i appreciate your service to our country and thank you for your contribution. i know that you would say as well that that is something that has been a great part -- a great part has been the work that you have done. i want to compliment the people that work with you.

11:21 pm

you study this. you spent time really looking at the big picture and had the chance to sit back, maybe more than many of the people here in congress have. and you made a comment. unless there is dramatic and quick action, we will head down a path. that is a very disconcerting observation. what do you mean by dramatic and quick action? what you think we need to be doing here in congress to protect against the kind of concern that you have identified in your testimony? >> first of all, thank you for your kind comments. it is certainly true -- i am the one that is to set the table and take the credit for our successes and plan for our failures, but it does not happen without the people that are banned senior staff. we have all benefited.

11:22 pm

what i was referring to is that i think we have to stay here within the realm of the possible. i could go back and said that there are certain things that could have been done with dodd- frank that could have made this a better protecting against too- big-to-fail. but in the realm of where we are today, there is a path that has a better chance than most of succeeding and that is the one that is being advocated by sheila bair, the outgoing chair of the fdic. it is not a very dramatic departure. it is just fulfilling the mandate of dodd-frank. what she has said is that part of the proposal is the living will where the banks are required to come up with a plan for how they will be resolved in the event of a financial crisis. and she cannot was say it -- with something, saying it over

11:23 pm

and over again, which does not seem to be very controversial. in order for us to carry out the mandate of dodd-frank, in order for us to really address today to -- address to-big-to-fail, they need to be resolved in a meaningful way and we need to use the powers of dodd-frank to simplify and shrink those institutions. what is remarkable about this is the deafening silence with which it has been met by the other regulators, the other members of the financial stability oversight panel, including secretary treasury timothy geithner. ultimately, they are too complex. they are too large. i think that chairman greenspan, famously at the beginning of this crisis, said that too-big- to-fail means too big.

11:24 pm

it is not just too big. it is a good place to start. it really does appear that what is happening with the chairwoman suggestion is a regulatory game of running up the clock. they say nothing. they do nothing. and the bottom line is that she will not able to institute those changes before she steps down during the course of the summer. those plans will not be coming in a manner of six months. it could be a year before anything happens. so what would be an example of dramatic change? how about a strong endorsement from the secretary of the treasury, from the chairman of the federal reserve and others that chairman sheila bair's suggestion will be adopted? perhaps this could help to away at the market's perception that resolution authority is somewhat of a joke. if you look at the language that moody's used at rejecting the idea that dodd-frank would work or somehow and too-big-to-fail,

11:25 pm

that this resolution of party is going to work, it is striking language. it is not just a passive projection. it is a complete rejection. >> moody's has included in their analysis the idea that the government is actually going to bail out the banks. this is part of the problem we're looking at. >> absolutely. there -- that this is going to happen. it is a it -- they reject that this is going to happen. it is a minor first step. but instead of issuing what is basically empty statements that this will and too-big-to-fail as we know it and we will never have to bailout anybody else again and there are provisions in law that i have heard that says there will never be a bailout, let's start with unarticulated plan similar to the one advocated by chairwoman sheila bair that says, ok, this is how we will do this. we will simplify and shrink

11:26 pm

these institutions so we can have a credible response to the markets that we will not bail them out. right now, the empty rhetoric, the market is not buying it. you can actually measure whether or not your statements are effective or not. all you have to do is look at what the credit rating agencies say, look at how much cheaper the benefit is, how much cheaper it is for the banks to raise capital. there things you can actually look to. while it is unfortunate that credit rating agencies have so much power and influence, that is the sad reality of where we are today. i think there has to be -- it has to start with an increase in rhetoric and then it has to be backed up by demonstrated action to fulfil those rhetorical promises. right now, we do not have any of that. what we have is a lot of discussion about endless roll- making that will accomplish some goal, a real sense of incrementalism.

11:27 pm

we will do a little bit here and a little bit there. i personally believe that chairman sheila bair's approach is a better one. >> the gentleman's time has expired. >> thank you, mr. chairman. >> thank you so much. i could not help but think about the fact that, come june 25 in my district, 40 miles from here, people will march into a room, to a conference of the preventing foreclosure. they will march in with tears, literally, about 1000 of them. and they will face some very difficult situations. they will finally get a chance to sit down with some lenders and tried to come to some resolve with regard to modifications. many of them will be lied to. many of them have been lied to.

11:28 pm

they have been playing games with them. a lot of these servicers, as if they were fools. when i read your editorial this morning, i was very impressed. we just voted yesterday to end the have program. i know how you feel about it. many of us feel the same way. but when you and the program and there is nothing to substitute, nothing, i am wondering if that is a good idea. i am just curious. >> as special inspector general, it has always been my position and continues to be my position that tarp made a promise. congressman, i don't to presume

11:29 pm

anything about you or your decision to make your vote, but, for a lot of progress as that i have spoken to, members of congress, the reason why they voted for tarp, one of the really things that convinced them to vote for what is essentially a bank bailout was this promise to preserve home ownership. >> you are right. that is one of the reasons why i voted for it appeared >> this is part and parcel of tarp in my view as the need to save the financial system. i do not rank them. i put them side by side. it was just as important to do with home ownership and deal with the foreclosure crisis as it was to deal with the banks. i believe that then it is on par. i look at the disappointments, the broken promise of the hamp program.

11:30 pm

i do agree with you that we cannot just abandon that goal of tarp. and also can defend, for those who voted for termination of -- i also cannot defend, for those who voted for termination of hamp, because they had the opportunity to make a difference. why has treasury not lived up to a different promise it made, the one it made in november 2009 to impose financial penalties on those servicers for not performing? why are we to use it to the program without a single financial penalty for performance? >> i need to get to one other thing. the reason why i started out the way i did, we can have all these discussions we want, but when i go back to my district and i know members on both sides of the aisle, when they go back to their districts, but some of

11:31 pm

them may not see these folks. but there are a lot of americans suffering. if we basically cut the money for carrying out dodd-frank, do you have an opinion on that? because that is what is happening. >> i come from a law enforcement background. i spent eight years at the u.s. attorney's office. during budget freezes and hiring freezes, i think you for your generous support during this crisis for our resources. but those budget cuts and freezes have a direct impact on the ability of those offices to put people in jail, to lock people up, to hold people accountable. >> but does it also have an impact -- you said that you know how the market is viewing dodd- frank. he talked about the possibility that dodd-frank operates and

11:32 pm

they look at it and say, you know what? we are not so worried about it because you said to-be-to-fail. but could it be that they see an effort to take the money from out of these agencies so they can properly enforce and carry out dodd-frank? >> it may be part of that perception issue. the bottom line is that the regulatory agencies that are charged with natalie implementing dodd-frank, but also law enforcement goals and enforcement goals -- i am thinking specifically of the sec -- when you take away funding, it may be that they will reallocate resources to dodd- frank. but as an agency, there will be able to accomplish less as far as enforcement is concerned and in implementing dodd-frank. i am not here to wade into the politics of a budget battle but

11:33 pm

it is simple. i have seen it over and over again. when spending freezes hit, it has a direct impact on enforcement. that is a reality. >> "the wall street journal" article noted that the department's seem to be drafting bills to take apart this reform piece by piece. what do you think about the funding or dismantling dodd- frank and what it has on the perception of the markets? >> i am not sure the impact is, in part because of the political realities of a decisive government. i have not traced anything or seen anything or heard anything that directly links that. of course, if the agencies are cuts deeply to the bone that they are unable to implement for visions of regulatory

11:34 pm

reform, that will have an impact. but i think the far greater impact, frankly, is the lack of political and regulatory will in staking out how they will use that authority since they have all the resources to really take on the issue of too-big-to-fail. unless we see that shift, i think that will have a far greater impact on market perceptions. >> i think the ranking member. >> thank you for being here this morning. i have one general question and i would like to just ask a couple of questions about some of the comments you have made already. would you agree that tarp picked winners, perhaps letting weaker entities survive. -- survive? if so, do you think that may have been a misallocation of

11:35 pm

funds? >> when you look at tarp as a whole, the lack of transparency in the program has led to the very fair criticism that, at times, tarp may have picked winners and losers. generally speaking, when we talk about the different truck programs -- there are 13 different tarp subprograms. we often think of a tarp as a monolith. we think of it as a capital purchase program, which, by very domitian, picks winners and losers -- by very definition, picks winners and losers. but there was, in fact, a process in place that depended mostly on the banks'regulatory ratings. on certain occasions, we did audit work on this. certainly, there were winners

11:36 pm

and losers picked. tarp did not have a perfect record. there have been a member banks that were supposedly healthy and viable that failed. there were others that were deemed healthy and viable and, a month later, needed to get a tremendous amount of additional support like bank of america and citigroup. i am understand that concern. on the flip side, it probably would have been inappropriate for tarp to give money to all institutions that came to the window. part of the importance of giving out text-- giving a tax payer money is to make sure that they were viable. based on our work and our reporting, it was incredibly difficult. there was a real sense of panic. they made some mistakes for sure, but i do not think they were intentional in anyway. they tried to get it right. they just did not sometimes.

11:37 pm

>> i want to go back to a comment for when you were responding to our chairman. you mentioned that unless treasury and the regulators use their authorities -- you mentioned that some of the '30's they already have -- that we -- some of those authorities they already have -- we will experience the same or worse. can you explain the authorities you are referring to and if they exist prior to dodd-frank. >> caps all leverage, capital floors are examples of things that have been around for a while. i think that what dodd-frank does is that it really forces an entry point for using those types of mechanisms anticipatory. this gives us an entry to

11:38 pm

evaluate the largest banks that were deemed systemically significant and evaluate whether or not it really could survive or whether the system could survive their failure. that is the key to any resolution plan, which is to take what ever it is, as chairman sheila bair suggest, and putting it through a reality check. if it does not meet the reality check using those tools, either spin off certain businesses, shrink the company, simplified organizational structure -- if you look at the lehman bankruptcy and the 3200 something different entities that were hopelessly complex and makes resolution difficult, i think that is a good start. of course, we have to remember that one of the limitations of waiting too long -- in other words, we do not use the authorities when we get the resolution plan prescriptive lead before the next financial

11:39 pm

crisis -- even our best intentions may not really work. in an era of a financial crisis, that is when all these institutions are suffering similar threats at the same time. it will be very difficult to execute some of these resolution plans. how do sell-off a large business job as part of a resolution if there is no one to buy it because the other entities are going through the same stresses of the financial system collapse? i think that is what secretary geithner meant when he said to mus did dodd-frank help? we need to do exceptional things again because, even with the best intentions, the reality of that the shock to the system will require -- as long as the banks are too big, it will require, again, extraordinary intervention. >> thank you very much. >> mr. welch. five minutes.

11:40 pm

>> thank you very much, mr. chairman. if i understand it, you say that dodd-frank has not succeeded in making the market believe that it has addressed this issue of too-big-to-fail. >> the implementation of it has not succeeded in convincing the market. >> is a because of the regulatory provisions -- is it because of the regulatory provisions? >> yes, some of that put the responsibility on the regulators to edelman the necessary changes and send the right messages to market. >> so we would have been better off with congress testifying what were the guidelines and what were the parameters within which these large financial institutions could operate? would that have been a better

11:41 pm

approach? >> it would have been a more effective approach if ideas like the amendments in the senate to dog frank -- to dodd- frank would put such as caps on the larger institutions. if that had passed, it would have sent a clear message to the market. >> that is simple. >> you would have relied lot less on the regulators if that were included. >> when we get into the regulators, of course, having a budget challenge in this country and in this congress, if we are cutting the budget for, for instance, the sec by $25 million, how does that affect -- what kind of signal does that send and how does that affect the ability to actually supervised the regulations that would apply? >> according to the sec, it would have a very direct result.

11:42 pm

it would inhibit their ability, according to chairman shapiro, of being able to implement the requirements that they need to do under dodd-frank. >> in your independent capacity, that offer makes sense to you? >> there is no question. when you are a regulatory agency, a law-enforcement agency, and you have fewer resources, you have to make cuts across the board. everything suppers. that will suffer. enforcement will suffer. >> the same thing with the consumer financial protection board. dodd-frank calls for an independent watchdog. that would be independent. it would not be advocating for the interest of the large financial institutions. it would be advocating for the interest of consumers. the sierra provision, the continuing resolution provision, which cut that down by 40%,

11:43 pm

from $143 billion to $80 billion japan which have the same response to the budgetary cut -- $80 billion. would you have the same response to the budgetary cuts? >> having been fortunate enough to work with elizabeth warren as she was the chair of the congressional oversight panel, i would certainly take her at her word that this would impact the ability to go forward. press one of the points of this hearing is that there are some legit -- >> one of the points of this hearing is that there are some legitimate questions if tarp was working. it is not clear what the consensus would be on this committee and if we want to be tougher on the too-big-to-fail policy or not. that is not part of it. but let's assume that we did have a view that was shared across the aisle, on both sides, where we did want to protect the taxpayer from a future bailout.

11:44 pm

what would do it -- what would be your recommendation for congress to do for protection against another bailout? >> step one is working within the tarbell that has already passed. that is to exert as much pressure as you can on the congressional oversight panel, on secretary geithner to fulfill the promise and to not take an approach and lookt at the recommendations of chairwoman sheila bear. getting rid of that subsidy, getting rid of the economic advantage that the bigger banks have over their smaller counterparts, whether it is the implicit guarantee, the increased credit rating, that has to be a goal. this is the remarkable thing

11:45 pm

about too-big-to-fail. perception matters. perception is as important as anything else. it is unfortunate that the credit rating agencies still have some much influence over things. but that is reality. we have to take those perceptions head on. many to figure out how to use the tools we already have to do with that perception and not just, i am sorry, ignore the advocacy of chairman sheila bair and others who have strong ideas about trying to get this to a place where these banks no longer enjoy that subsidy. >> i would be happy to -- i thinwe to -- i think we agree that we want to and 2-big-to-fail. but i know that has been your advocacy in your time in congress as well as mine. the bill of goods that some of us saw coming out of dodd-frank is that it would prevent too- big-to-fail. >> i appreciate that. as the chairman knows, i voted

11:46 pm

in significant part because of the testimony of mr. borofsky. in so much as we can find a way to work together, i agree with your statement. >> i thank the chairman for his advocacy. we do not always agree, but you have a great way of reaching out and try to find consensus. with that, i yield five minutes issa.nator eis >> thank you. if we can get to some bipartisan discussion where we agree to a number and say, if we need to add sec, or some of the websites and so on that are also being cut and back them up because

11:47 pm

they save us money, then i think then we can find those offsets. i think that the chairmen agreed that hamp was an awful lot of money that was not meant to ruin people's credit rating. i am concerned about where we make the cuts. i would hope that, in the very near future, we talk about the need to make austerity moves and then begin to say where can we find multiple votes for something by putting things back. you mentioned the sec. i am concerned that many of the summit activities that we have on a bipartisan basis been investigating -- i think we need to have the access that, quite frankly, dodd-frank, with bipartisan support from this committee, almost got with

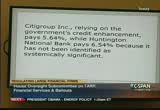

11:48 pm

transparency. we still have to get back to getting that transparency into what was dodd-frank. if i could throw a slide up, i just want to go through a couple of these. it illustrates probably the most important point you are making today. it is the 2-3 step credit rating increase. go to the next slide. real examples -- wells fargo, if their cost of money is 4.81 vs -- if goldman sacks, often vilified here, but if their cost of money is just under 5% while national city is over 6%, that is not the three-quarters of a point you're talking about. barclays bank is that 4.39% vs. the tnt -- bb &t.

11:49 pm

huntington national bank has 6.54%. let me ask it to you in a different way, as a former businessman. if i am among the most creditworthy companies, the fortune 500, down to small companies that simply have healthy balance sheets, is there any reason in the world that they will not migrate to the largest banks when the largest banks can make a profit of nearly a point cheaper than their competition? in the pure cost of money, will this not move the more creditworthy to the big banks while leaving little banks with higher rates and being forced to take what is ever left behind? >> absolutely. let's say your deposit money at one of these banks. you go beyond the fdic's limits. do you not want to have an implicit government guarantee

11:50 pm

of too-big-to-fail behind your deposits? from an ethical and point of view, you may not want to support these institutions because of this implicit government guarantee. but, as a businessman, how can you not take advantage of the fact that you're getting what is essentially free deposit insurance based on the implicit guarantee that the government will bail them out? what does that do? it makes them bigger? it makes them even more systemically important. it is a downward spiral. and for the smaller banks, it gives them incentive as well bid we need to get bigger. we need to get on the gravy train. we need to raise money more cheaply because of the implicit guarantee. it is a complete perversion of the system. >> that brings up a point that i want to make sure the committee focuses on. if we do not change where we are today, the five banks that represent 50% will be seven banks that represent 80%.

11:51 pm

through mergers, the banks will get these rates by being big enough to be not too-big-to- fail. that would be my approach to get my business away from the big 5. >> it is a real danger. there are some provisions in dodd-frank that prohibits concentration of 5% of all deposits. one of the things we talk about is lehman and was it not a good example of the government not stepping in? but so much of the incentive of allowing women to fill was a lesson that we need to get bigger than women because we need to make sure that we're big enough so that is a bigger than lehman because we need to make sure that we are be enough -- we need to get bigger than lehman because we need to make sure that we are big enough. >> thank you. >> is a pleasure to have you

11:52 pm

here. when i was a kid growing up, i remember commercials -- in the avis commercial -- "we try harder because we're no. 2." all of a sudden, number one seems to be a guaranteed by the federal government. whoever is no. 2, good luck because you can try as hard as you want. with community banks, if we see what happens when you have seven banks taking 80% of the market, it seems to me that there is only an incentive for community banks to merge with or be acquired by the too-big-to-fail banks. is that the president we're setting up with a the tarp package? cedent we aree presiden setting up with the tarp package? >> certainly, consolidation and

11:53 pm

consolidationlars could be a bar product -- continued consolidation to be a byproduct of where we are. >> the community banks to be serving most of our businesses in terms of loans. it could give them what i think would be an opportunity for the too-big-to-fail banks to dictate more policy and restrictions. >> less competition as never before the consumer. the notion of having more political power almost seems and have a look at this point, but it could have them. >> systemically, as a result of the tarp package, has been anything to change the way we do business to avoid ever having to have another tarp package passed by this congress? >> in many ways, the way it has been executed and the way it has

11:54 pm

a legacy of increased moral hazard, it has made a lot even more likely. unless we deal with this too- big-to-fail problem, the increased size, the increase interconnectedness, the fewer number of large institutions, all contribute an elitist to where the too-big-to-fail this will be even bigger and their failure even less conceivable as possible. >> is it possible that the precedent set their that such tarp packages would be considered for non-financial institutions, insurance companies? we saw that with aig. this does not set a precedent that goes beyond assisting financial institutions and any entity that may be deemed too- big-to-fail regardless of what their commercial purposes. >> the tarp was not limited to

11:55 pm

banks. you have to aig, the automobile industry -- that is part of tarp's legacy, the extending of moral hazard. >> in any of your class is, would you -- classes, would you consider changing your business plan to include a path to where you can now be required or be guaranteed by the federal government because of the precedent that has been said in the last couple of years? >> unless we make that so painful and really address it through our regulation, again, right now, it is a pretty good place to be to be too-big-to- fail. >> i yield back. thank you. >> i ask unanimous consent to

11:56 pm

have two additional minutes. will also give the gentleman from vermont, mr. welch, two minutes. >> allred. >> thank you. i have spoken with you about this fall business lending fund. this legislative creation that does not have oversight from your office, can you talk about the small business lending fund and the impact it has especially on these tarp banks, these small car for banks that are still within the program? >> commerce enabled treasury to refinance, if you will, really move banks off of the tarp leisure. - ledger.

11:57 pm

we made a series of recommendations to treasury, which is to reject it, to help protect the american taxpayer as those banks move from the tarp ledger. there's less oversight. there are less protections come up capital protections for the taxpayer. we have made a couple of recommendations and they have been rejected. it is not entirely within our jurisdiction on this issue. we have jurisdiction over the sale of troubled assets. hear, the sale of preferred shares of stock which are being sold from government entity and purchased by another government entity is very much within the confines of our gestation period for that, we have requested an audit. -- confines of our jurisdiction.

11:58 pm

for that, we have requested an audit. we were told that we needed to hold off because treasury general counsel has to decide whether or not we have the right to conduct an audit of the exit of banks from tarp. i have not written a letter. i have not written -- may big deal about this because, frankly, i can add even conceive that there will come out and suggest that the very clear intent of congress that we have jurisdiction of tarp banks will not be there because the money has not been funded in to this program yet. we do not have a sense of immediacy yet. but if there is some those are legal construct that they adopt and suggested that we cannot do this, i certainly hope that my successor will immediately bring that to this committee's attention. this is a very important area because of the potential for the taxpayer to get a raw deal as a

11:59 pm

top banks exit tarp and go into fdlf. >> thank you. i yield 2 minutes. >> on february 25, i requested that your office conduct an audit on homeowner complaints. can you tell me what is going on with that and when we can expect to have some results? >> i just got an e-mail that has the preliminary numbers. we're going through more than 2500 hits on our hot line. what has been helpful is it has helped us organize their hot line hits. since we have gotten your letter, our staff has been going through our hot line, literally and tree-by-entry and pulling them together. i got -- entry-by-entry and pulling the together. i expect we will have it to you before too long. i cannot give you an exact date.

12:00 am

you you're walking out, cannot dump a commitment to the people behind you that you cannot fulfil. >> ok. let me ask you this. one of the things that concerns me is that we will -- as you move on, the question becomes -- i would say what would your response be to what they're going to say in some way or another? it sounds like you made some reasonable recommendations and mr. masaad said he would be retooling. have you seen evidence of that?

12:01 am

why wouldn't the administration accept your recommendations -- some of your recommendations? i am curious and there is -- i am curious. >> there has been no retooling. yesterday which was on the date of the vote, there was an announcement. it was an op-ed in politico. they're going to two years later, almost 18 months after the promise to impose financial penalties on nonperforming servicers, there will be a plan. i read the op ed and it was brought to my attention. it sounded like a gimmick. they will give servicers grades and withhold payments based on that great. ok. it is some movement in that direction. although again, words, i do not

12:02 am

put a lot of faith in words given what we had 18 months ago. it is action that matters. i did what you would -- i would normally do. i reached out to treasury. give us the back of for this. let's evaluate. i am asked the question today, i can give an opinion about whether this will be effective, with the construct is and the response, first and got no response. we got a response, we can tell you because we do not have any other policy or plan other than what was outlined in the opposite. this is ready, fire, aim, all over again. this is one incident of potential retooling. meeting our recommendation. almost everyone's recommendation to start holding the servicers accountable financially. i am hopeful that this is better late than never as opposed to too little too late. a ultimately, where it's at this

12:03 am

point are just words. after the broken promises, we need to see some action on this front if we're going to get servicers to be held accountable for their terrible and abysmal performance that treasury acknowledges. >> thank you. >> we appreciate your testimony. your candor, your ability to react to a variety of questions. too often in congress, we see the person on the other side of the panel as more sport. it is interesting to have someone who was on the other side of the panel who is of a sporting mood. you are willing to react and answer the question posed to you. to often, in this place and around washington, is not about answering the question, it is about what you want to answer. there have been frank and

12:04 am

forthcoming, very open in answering the question supposed to you even when they're not convenient. we appreciate your service to your government and to your country. thank you for a time and testimony. most of all, thank you for your hard work. >good luck to you and your future endeavors. this committee will be in recess for five minutes.

12:05 am

the committee will come to order. mr. masaad, thank you for being here. it is the policy that witnesses be sworn in. if you will stand and raise your

12:06 am

right hand. do you solemnly swear or affirm the testimony you're about to get will be the truth, the whole truth, and nothing but the truth? >> i do. >> but the record reflect the witness answered in the affirmative. with that, we will recognize you for five minutes and you're written testimony will be entered into the record. we will have some questions from the panel. >> thank you. distinguished members, thank you for the opportunity to testify. you have invited me here to address whether the perception some institutions are too big to fail persists despite the passage of dodd-frank. the quarterly report suggested legacy may be's

12:07 am

the too big to fail institutions. moral hazard is a real and significant concern. to suggest this is the main legacy confuses a response to a crisis with the need to fix the flaws in a regulatory system. t.a.r.p. was necessary and it did what is supposed to do. its legacy is that a combined with other government actions helped save our economy from a catastrophic collapse and may have helped prevent the second great depression. the lesson we learned from having to take these actions was to better protect ourselves against future crises and to do with the moral hazard issue, our system needed to be fixed. today while more work remains, we have taken action to do just that. we have taken steps to address the moral hazard associated with the fact that t.a.r.p. and other interventions were necessary to address the problem.

12:08 am

19 months after it was enacted, congress passed the dodd frank act. dodd-frank contains three main elements. first, it gives the government of 42 shot down and break apart firms whose failure might threaten the system. it does so in a way that protects the economy while ensuring large financial firms bear the cost. it provides as with the tools to insure no firm will be insulated from the consequences of its actions are protected from the year. it makes clear that taxpayers must be asked to bear the cost of a financial firms failure. dodd-frank creates a framework for identifying and responding to rest in the financial system that creates the financial stability oversight council and the office of financial

12:09 am

research. it is charged with responding to emerging threats and promoting market discipline. ofr addresses the critical need for more standardized and useful data. dodd-frank requires regulators to impose substantially stronger provincial standards, risk-based capital standards will be stronger. complex firms will have to hold more. dodd-frank requires that certain large firms undergo regular stress tests and requires living wills. it restrict risky activities by banks such as proprietary trading as well as the excessive growth by acquisition of the largest firms. it sets a clear path for. we have made progress to implement its provisions but there is more work to do. the financial markets are watching this progress which underscores the importance of

12:10 am

the implementation. let me turn briefly back to t.a.r.p. a strong area is unwinding the assistance that had to be provided. since the last appeared, t.a.r.p. has continued to make good progress. we have reduced the dependence. we expect to receive $7.40 billion in repayments and taxpayers will have recovered two ordered $51 billion compared to the two ordered $45 billion invested. that will be the gain to the taxpayer. with the repayments over 70% of the amount has been recovered. the ultimate costs will be far less than anyone expected. the cbo estimated the costs to 8

12:11 am

$19 billion. it is one part of the actions taken to respond which included support for fannie mae, freddie mac, the federal reserve actions and guarantees money market funds and bank debt. it is important to look at the cost of these measures. the latest estimates of these interventions shows they are -- it should be a small profit when we look at those actions. this estimate does not include the stimulus measures and does not include the cost to our economy. jobs were lost and businesses fail. household wealth declined and tax revenues fell. that would have been worse without the emergency response. thank you for the opportunity to testify. i welcome your questions and let me say i am happy to respond to any of the matters that were raised whether it is pertaining to dodd-frank or other issues.

12:12 am

>> thank you. i recognize myself for five minutes. there are a number of questions dodd-frank raises. i read your editorial against my legislation ending the program. we do not have to litigate that. we won the vote so i am fine with that. we had a bipartisan vote as well. i hope that sends a strong message to the overseers of the program. the status quo is simply not acceptable. destroying credit scores, taking their savings, it is not a responsible program in order to help half a million people.

12:13 am

the people who are brought into the program and given verbal modifications of their mortgages and are kicked out of the program at the end of the day. the recent report was 700,002 ordered 40. we appreciate you releasing those numbers but it is not acceptable. we do not have to really get that. i want to raise a question i think is interesting. use of the taxpayers will not be on the hook for future bailouts. can you explain how you justify that under dodd-frank? >> dodd-frank provides taxpayers will not fund any bailout. it gives the authority -- >> how does it do that? >> it gives authority to fdic to liquidate and non-bank financial

12:14 am

firm that is threatening the system and to oppose those costs on creditors and shareholders, including the ability to clawback those costs and to the extent those costs cannot be imposed on creditors and shareholders. there is an assessment after the fact on large financial institutions. >> you disagree with the assertion that dodd-frank and robust, the comment that in the event of the next crisis we have to do extraordinary things beyond the scope of the dodd- frank legislation. >> as i testified before, the secretary's statement referred to the fact that it is difficult to predict the shape, the nature of a crisis. you may have to take extraordinary actions but he was referring to using the tools of dodd-frank. >> interesting. ok. another question i have.

12:15 am

is treasury in terms of looking at financial stability, are you looking at the interconnectedness of our financial markets across regulatory regimes? for and regulations and how they are moving forward. is there going to be, speaking to market participants. they see an opportunity for regulatory arbitrage and to make money based on the fact that other european countries are behind in terms of changing their financial regulations. is this a concern? >> absolutely. it is a good question. thank you for raising it. one of the important things is to work with foreign regulators to -- >> are you doing that? >> yes. there is work going on to do that. the dodd-frank law provides for

12:16 am

that. >> i know it does. how was that going? is that progressing? how is it progressing? what are you doing? >> there's a lot of work going on by each agency. as you know. >> i know there is a lot of work going on by each agency. you are stating some obvious things. it is part of the treasury tact and i have seen you before. i call my own time so you need to answer the question. >> i will be happy to provide you with details about that. i do not have them at my fingertips. it is not my responsibility to coordinate with our international friends on those regulatory regimes. it is my responsibility to implement t.a.r.p. i would be happy to get you a detailed response. >> it does not entail looking at international regulatory regimes is when i am trying to understand. i will move on.

12:17 am

it is fine. the financial stability oversight council. which is a creation of dodd- frank entails regular sitting on a council together. each regular has their own staff. is it your view in terms of preparing for this, how this council will operate? how their meetings will occur, where they will occur. is this being driven by the treasury department? >> fsoc is chaired by the secretary of the treasury and it has a number of members. 10 voting members as well as non-members. it meets periodically and it is promulgating rules. it is a lot of activity. it requires the coronation

12:18 am

across all agencies as you know. >> i do not believe i said that financial stability does not entail looking at international regimes. i think i said the contrary. i would be happy to have you details on what is going on. >> she said it was not york responsibility. >> that is correct. my responsibility is t.a.r.p. i will recognize mr. quigley for five minutes. >> thank you. good morning. questions this morning were brought up earlier about the community banks, the relative disadvantage. are you in a position to talk about the comparative disadvantage many of those banks, many in my state are at and what can be done? >> that is an important question. we have to have a thriving

12:19 am

community bank sector in this country. we have taken a number of actions to do that. we funded the obama -- the it obama administration did not provide funds to large banks. we provided funds to 400 small banks and 60 were funded out of the program. treasury push for the implementation of the small business lending fund to provide assistance. the differential you referred to is important. dodd-frank provides us with tools to address that. it allows us to impose tougher standards on the largest banks. capital standards, leveraged standards, liquidity standards. there is a lot of work to do to implement that but it does give us some tools to adjust the problem. -- addressed that problem. problem.ess that >> could you detail some of

12:20 am

those? >> some of our banks do not have access to capital markets. that is why we have been able to see a lot of the larger banks have repaid t.a.r.p. funds and some banks have not. we are continuing to work with them. is capital under a tart.a.r.p. not required to be repaid. the fact that we funded a lot of those banks has help them weather the storm. >> perception in my state is that as simplistic as it sounds, you have bailed out the big banks and shut down the small ones. if you are in my position, how do you respond? >> a good question. i think what we say is in fact under t.a.r.p., we provided capital to any small bank that

12:21 am

was viable. we ended up providing that overall, 650 banks. we're continuing to work with them. the issues you raise as to whether big banks have an advantage. dodd-frank is meant to provide us with tools to level the playing field. it needs to be fully implemented. >> a lagered discussion at some point. let me shift gears. march 21, a report that goldman sachs and others are skirting the volcker rule by saying it does apply to long-term principal investments. what has reaction to that then? >> i am not familiar with the particulars of implementing the volcker rule. i would be happy to get your response. >> thank you. i yield back.

12:22 am

>> this is not the time -- you had identified one of the things you would do is to try to be responsive to any comments that were made by the gentleman who testified before you. he raised an issue which was a question i think your general counsel was looking at, the right to conduct an audit of the exit of banks from t.a.r.p. is there any reason that should be a question? what is your position as to the authority of the inspector general to audit that process? >> thank you. it is a good question. the issue goes to whether

12:23 am

sigtarp or the inspector general has jurisdiction or what their jurisdiction is. i respect both are in total to those opinions and i defer to the judgment of the general counsel as to the proper jurisdiction between them and that is what is going on. >> you have a willingness to engage in this activity. if it is determined the inspector general from treasury is the entity by you, are reassured that the inspector general from treasury would conduct that same on it? >> it is not my determination. it is a question of interpreting what the law requires and provides for. both as to the small business lending fund law as well as t.a.r.p. both the special inspector general's office and the inspector general's office are very excellent operations that

12:24 am

have conducted a thorough audits and i would be happy to work with both of them as we have. that is an issue that will have to be resolved. thank you for observation. i did not understand why there would have been any reluctance. as we look at the larger question, not just where we have been because there is a collage of analysis and information on both sides, much of it credible about the successes of t.a.r.p. there is an issue where we're going. part of the problem is the unintended consequences with the bigger banks getting bigger. a lot of the oversight going toward the institutions that were not the target of this initial effort. what i am concerned about is the perception that now we have

12:25 am

rating agencies that are factoring in the likelihood that somebody is going to step in to cover these banks in shoring up their position. i am dramatically concerned about the consequences as ben bernanke said. it creates a limited market and limits market discipline in this context. how do we check the ability to be assured we are not going to see this again and one of the factors i see you have been looking at has been the idea of the living will. what is going to happen in practice with that living will? are we and forcing this, are we requiring that an effort be made to compel these organizations to explain how they will get out of it? >> absolutely. it is a good question. i was rather surprised by the

12:26 am

comment that somehow treasury was opposed to this. it is a requirement of dodd- frank. of limitation of living wills is left to the fdic and the federal reserve. they have until january 2012 to work on it. it was part of the proposal that treasury made and we have backed the concept the entire time. you are right, that is a critical tool on how -- and how thoroughly it that is enforced and how thorough those plans are will make a critical difference. in terms of the rating agencies, they're watching this closely. they should. again, have made it clear that what they're doing is monitoring it. they are seeing -- >> they are making calculations and the calculation is we're reading the banks and giving them a preferential position with respect to the market based on their confidence that someone

12:27 am

else will step in. >> that is correct and they are doing that worldwide. they have said we're closely monitoring the situation to see how these resolution regimes are implemented and to see if there is the political will to ensure the there are no bailouts in the future. >> what would that take? what should be requiring for them to people to pass the scrutiny of that living well analysis? >> where at this early stage of the implementation. the law was passed eight months ago and to say it is not going to work, it is like saying we passed the securities act in 1933, because they cannot fix our markets within six months, they did not work. we set up the sec and took actions and we have the most vibrant and robust capital markets. it is like saying we passed the

12:28 am

civil rights act and it did not end discrimination. there is time needed to implement. we're busy working on it. it involves many agencies, not just treasure. i will come the suggestions if he has suggestions on how to implement it. i have not heard any specifics. >> thank you. i turned to the gentleman from maryland. >> thank you. let me ask you this. you have heard the testimony earlier. >> i did. >> you talked earlier, you said there would be some retooling. basically if i were to sum up what mr. borowski said,

12:29 am

it is late but at least you are aiming in the right direction. he did not seem to have confidence based on the past that your department is going to do very much of anything. even under the threat of demise of the program. i am wondering what is your reaction to that? >> thank you for the question. my reaction is to be puzzled. i felt like there was strong criticism but i did not hear specifics. sigtarp made recommendations to us. we have implemented 14. the ones we did not would have made it harder for people to get assistance. it would have required us to thumbprint anyone and would have

12:30 am

required more documentation about income, comparing their income to when they got their mortgage. other things like that. the last recommendation was in april of last year. lately, he said the program is a failure but we have not seen in thesanything specific. we are expanding our compliance reporting and we will withhold incentives. on that, what we did from the outset was we had a very strong compliance program to get servicers to fix the problem. there was not -- we only pay money when they enter into the permanent modification. there were not entering which is why we focused on remedial actions. >> there is a lot of frustration on both sides of the aisle. the question is, what can we do

12:31 am

pass the conversation to affect more people? is there something we need to do differently? i for one and many of my colleagues voted against the bill yesterday to and the program. most of us said to ourselves and each other treasury has to do better. this is real. i am wondering, what is going to happen? we cannot keep going down this road to where we're going. there are people suffering and with all that money out there, it gives the opposition more ammunition to not only destroy the program, but also not replace it with anything. that goes against everything that we're trying to accomplish.

12:32 am

i want to know what direction is. >> you are right. those people who want to end the program have not offered any alternatives. we continue to look at ways we can improve it. it is a difficult issue. we have a lot of people who spent time on this and if there was a silver bullet, it is not easy. the program is continuing to help tens of thousands. it is affecting people indirectly through the standards that were setting -- we are setting. >> do we need to raise the standards? >> absolutely. we need national servicing standards and there's a lot of activity going on in that regard through the discussions on the foreclosure problems and otherwise and we will see that coming. we are committed to that. we have met with members of

12:33 am

congress about specific things that need to be in those national servicing standards. >> one of the things he said, there are the tools in dodd- frank but he said he does not believe that the administration has the will to carry it out. i want you to comment on that but on this other issue. if we take funds away from the budget, how would that affect the market perception? % but taking awayrcent tha funds would not be a good thing. we need to make sure we

12:34 am

vigorously enforce this. as to the comment, i do not know what specifics he is referring to. the implementation process is an open one. there are a number of rulemaking proceedings going on. if he has comments on those, he can make them. if he thinks certain things are not happening fast enough, he should point that out. >> thank you. >> thank you. the gentle lady from new york. >> thank you. thank you for being here this morning and a willingness to testify. i am looking at your opening statement. i wondered if we could flush out a couple items that are in your comments. in reference to dodd-frank, you listed three points for us. the first one is dodd-frank gives the government the authority to shut down and broke apart large non-bank financial

12:35 am

firms. to what extent, what is the scope of that? should we concern the government has the kind of power they can shut down a private entity? >> it is a good question. there is a process that has to go one. a determination that has to be made by treasury and the vote of the fdic and the federal reserve and consultation with the president. there are criteria that have to be met to do that in terms of when you can use that authority. those criteria include there is not another way to do with the situation. the firm does pose a threat to our financial stability and there are others. there is rulemaking going on to further explicate that. it is important for there to be clarity as to those rules. >> thank you.

12:36 am

the second point for identifying and responding to risk. that would tie back to the first point. there are -- are there benchmarks you are going to look for that will identify someone is in trouble and the government needs to take this aggressive action? >> there are standards that need to be implemented and fleshed out more. the key thing is that prior to the passage of dodd-frank, we regulated entities based on the type of entity and we did not have a comprehensive way of looking at risk to the system. that is what we have now. that is why this law is so important and why implementation is important. we can take proactive measures to impose provincial standards, whether it's the capital, leveraged, liquidity, which can limit for risky activities and there is a process where you

12:37 am

exercise -- you can impose restraints on firms. it gives us a lot of tools but they need to be implemented. >> going along with that gives you the tools. what is the concern of the government? many feel dodd-frank is an overreach. we want to prevent what happened but we want to maintain free market. at what point does the government step back and say we're not going to get involved? >> there is a balance and congress struck the right balance plan dodd-frank -- in dodd-frank and give us the tools. that is why in has to be implemented thoughtfully overtime. that may change of time as our financial changes.

12:38 am

>> one more question regarding your testimony. you talked about dodd-frank, you say "much work needs to be done." can you expand. there are 250 rulemaking that needs to be done and studies the need to happen. it involves efforts of many agencies, not just treasury or fdic but the federal reserve and the sec and others. that is the work i am referring to. a number of those things, -- have been done or in process. there is a lot more work to be done. >> thank you. i have one last question. the government is a player and referee. do you say a conflict in all of this? >> i do not think we want the

12:39 am

government to be a player in the sense of having interest in firms. that is why we're unwinding the program quickly and get out of the business of owning stakes in private companies. we have been successful in doing that quickly. the government needs to stick to a to roll of regulating risk and monitoring risk and taking action when firms pose risks to the system but clearly, we have to have a system where there is no firm that is too big to fail. and firms fail as a result of the actions they take. >> thank you. i yield back. >> the chair recognizes the gentle lady from new york. >> thank you and welcome to the committee. during the financial crisis, some firms became so risky and interconnected that their

12:40 am

failure was a threat to the broader economy. i know congress tried to address that in treasury -- and treasury dodd-frank.-- in can you describe what happened [unintelligible] number of experts looking at the riskiness of activities. the fsoc will make determinations about which firms opposed those risks based on their interconnectedness, their leverage, the nature of their activities. the work is ongoing. those determinations have not been made yet. there will be made by fsoc, which is comprised of all these

12:41 am

agencies. >> thank you. one of the factors that led to the crisis is the evolution of the shutter banking system. trading and sales of derivatives had grown to be a trillion dollar business but it became evident that people, the treasury, even the companies did not understand the scope, location of the risk of the size -- location of the risk and this size. it became billions oand it was o control or understanding. can you comment on what advances you have made on the derivative market and bring it into the light of day to ensure it can exist without posing a threat

12:42 am

to financial stability? " certainly. dodd-frank does provide provisions for greater transparency and regulation of the derivatives market. we did not have those previously. there is a lot of work going on in that regard. >> can you specify? >> i am not directly involved. that involves treasury. the sec and ftc. i will be happy to arrange that. >> the growth illustrates that federal regulators had failed to keep up with market innovation and development. regulation could not keep up with innovation and dynamic action taking place in the markets. can you ensure that dodd-frank and the regulations will keep pace with the innovations in the

12:43 am

financial markets? >> it is a good question. what it does is give us the tools to do that. we have to implement them. previously, we did not have a system where we could look at risk across our entire system. we regulated banks and had regulation of other entities. we have an entire shuttle banking system developed and we had all this risk being taken on by firms that were not subject to regulation. aig is a classic example. there was no federal regulation of daiichi and it engaged in derivatives that were destructive. we have wound that down and there is the reason they will repay the government every dollar we gave them. >> we heard testimony earlier and one of the points he raised

12:44 am

is the act did not reach far enough to address international firms that operate globally. -- are financial institutions at a disadvantage because we have regulation? many of these other areas do not. they do not have the capital requirements. they do not have the rest restraints, the oversight that american firms will be having. >> thank you for that. the international coordination piece of this is very critical. we are dealing in a global world. we have these large institutions who are not national. they operate worldwide. that is why the coordination is

12:45 am

important. it is going on and the federal reserve is involved and treasury. i would be happy to get you more details on what is taking place in that regard. congress could not legislate something that mandates what our foreign counterparts do. it requires us to engage in coordination and cooperation with them. >> the basel talks, where do they stand? >> that will result in higher capital requirements that will be phased in over time that are badly needed. many of our institutions are better capitalized today than their foreign counterparts. we need to phase in those tougher standards. >> my time has expired. thank you for your service. >> thank you. >> thank you. let me turn to the gentleman from in illinois.

12:46 am

>> thank you and thank you for your testimony today. let me ask you a brief question related to the insurance industry. i have heard from people who expressed concerns with how dodd-frank affects the insurance industry. insurers are heavily regulated, including an industry funded state guaranty system that helps secure policyholders in the event of an insurance company failure. most insurers are not engaged in significant unregulated interconnected off-balance sheet, highly leveraged activities. so designations such as systemically important would appear to be on warranted in this industry. overlapping and conflicting

12:47 am

roles between state and federal regulators adds a layer of regulation that would disadvantage these insurers and their customers. as you know in the event of another large financial company failure, companies with assets over $50 billion could be on the hook to pay for the resolution of these failed firms even though they exhibited no bad behavior of their own. insurance companies who will continue to be resolved in the existing state system are never resolved by the orderly liquidation process and yet have to pay to resolve banks and other bad actors in the financial industry. these costs will inevitably be borne by the consumer. if insurance companies are regulated at the state level, and if it is clear they do not participate in systemically

12:48 am

risky behavior, why do they have to bail out other failing financial service companies that do participate in this risky behavior? >> your question raises a number of important issues. let me try my best. where i would start is we have come out of a time when we did have a very large insurance company that was regulated at the state level but which posed huge risks to our system. it was not regulated beyond that. that was b.i.t.. we did not have the tools to do with it. its failure could have brought down our entire system. that has animated the provisions of dodd-frank that address the insurance industry.

12:49 am

i recognize your point. we have to make sure these provisions are implemented in a way that is fair to those companies that do not pose those risks and do not engage in those activities. that is a process that we have to focus on as we go for. fsoc is focused on those issues. we need to do this in a way that imposes standards and restrictions on those funds that pose a significant risk to the system while leveling the playing field for the others. >> you acknowledged with regard to aig, it was not their insurance business that got them in trouble or brought them down. it is a complicated question. there were things going on with their insurance business that did pose some risks. you are correct that aig was involved in a number of

12:50 am